ORIGINAL ARTICLE

RIBEIRO, Renor Antonio Antunes [1]

RIBEIRO, Renor Antonio Antunes. The role of the governmental internal audit in the new Brazilian federal bidding law (LAW No. 14.133/2021). Revista Científica Multidisciplinar Núcleo do Conhecimento. Year. 06, Ed. 09, Vol. 07, pp. 55-77. September 2021. ISSN: 2448-0959, Access Link: https://www.nucleodoconhecimento.com.br/business-administration/internal-audit

ABSTRACT

With the advent of the new bidding law, several guidelines for internal control were adopted, with the adoption of the three-line model. Thus, it is essential to act correctly by the second and third lines bodies for the accountability of management and for the fight against corruption. However, the law has inaccuracies and omissions in relation to the role of the singular Internal Audits – AUDIN of the entities of the municipal and foundational administration. Because of the amount of AUDIN and the materiality of public resources supervised by the internal auditors of these bodies, the main question is to know the role of internal audit units before Law No. 14.133/2021 (new bidding law). In fact, the general objective is to know the role of the singular internal audit units of the federal public administration, in relation to Law No. 14,133/2021, more specifically with regard to articles: 169, III; 8th, § 3rd; 19, VI and 141, § 1 of the new bidding law. The methodology consists of a descriptive research based on secondary sources and qualitative approach to analyze the legislation that deals with the internal control system, the three-line model and the internal government audit. As main results and conclusions, we have that the unique internal audits of the municipal and foundational administration, based on the Brazilian federal legislation, the literature and statements of positioning of the IIA, are always in the third line and have the role of providing evaluation and consulting in their respective organizations, in a way that is competing with the Compton of the Union – CGU.

Keywords: bidding, auditing, internal, control, law.

1. INTRODUCTION

This is the analysis of the role of internal audit units before Law No. 14,133/2021 (new bidding law), based on literature, international standards and Brazilian legislation on the internal control system, the three-line model and the internal government audit.

The relevance of the theme is related to the role of the internal government audit for the accountability of public spending and the prevention and control of corruption, as established in the Brazilian Federal Constitution of 1988 and current rules, considering the number of indirect administration entities and the materiality of the public resources involved, which need to be effectively managed and supervised. According to Law No. 10,180/2001 and Decree No. 3,951/2000, the Comptto-General of the Union occupies the function of the central body of the Internal Control System -SCI, with the other Internal Government Audit Units – UAIG acting as auxiliary bodies. In the structure of each indirect administration body, which covers regulatory agencies, foundations, municipalities, universities. federal institutes, we have at least one UAIG acting in the third line for the good and regular application of public resources in favor of society. Therefore, delimiting the role to be played in the GAUs is fundamental for the proper functioning of the SCI.

In the new Brazilian bidding law, the expression “internal control” is used to refer to both the second and third lines, which can generate future competencies conflicts and misguided action of internal audits in management and governance activities. Moreover, according to Article 169, item III of this law, the third line is integrated both by the central body of internal control, and by the court of auditors, an external control body, which may characterize a conceptual error in relation to the model of the three lines of the Institute of Internal Auditors – IIA (IIA, 2020).

This work is justified by the need to establish the action of internal control bodies, both in the second and third lines, in each mention in the legal text, in order to avoid conflicts, overlaps of actions or even the loss of independence of the internal governmental audit.

The objective is to know the role, if any, of the singular internal audit units of the federal public administration, in relation to Law No. 14,133/2021, more specifically with regard to articles: 169, III; 8th, § 3rd; 19, VI and 141, § 1 of the new bidding law.

Therefore, we will do a descriptive research, based on secondary sources and qualitative approach, to align the role of internal audit to the best practices and provisions of the relevant legislation, in order to frame the internal audit and management activity in its proper attributions. Given that the provisions contained in Law No. 14,133/2021 do not seem to be sufficient to define the role of the internal government audit in the management of bids and contracts, it will be necessary to resort not only to the provisions of Law No. 14,133/2021, in which control is mentioned, but also to the literature and federal regulatory basis related to the internal control system, government internal audit activity and the model of the three lines of defense.

In fact, we will raise some concepts from the literature on the subject, in addition to conceptualizing the internal control system according to Brazilian legislation, covering the Brazilian Federal Constitution and other legal provisions. Next, we will talk about the model of the 3 lines in federal legislation, based on the model of the three lines of the Institute of Internal Auditors – IIA (2020), and about the similarities and differences of audit and control. Finally, we will conclude the theme, in order to offer an interpretation of the provisions of the new bidding law based on the concepts already addressed in the literature, current legislation and publications of the IIA regarding the role of internal audit in the internal control system.

2. THEORETICAL DEVELOPMENT/FOUNDATION

The provisions on the performance of the internal audit and on the internal control system established in the IIA and COSO standards were incorporated by the most recent Brazilian legislation, which reproduced the model of the three lines of defense in several devices, including definitions on risk management, governance and internal controls. In this sense, we will talk about the main concepts adopted by literature and international standards, and then analyze the legal provisions on the subject.

The role of internal auditing is to evaluate the functioning and effectiveness of an organization’s internal controls, controls that are actions or means to verify that activities are taking place as planned. Maia (2005) argues that the internal control system contributes to organizational excellence with COSO (2013) as a reference for the internal control structure. For De Oliveira (2014), the internal control system is the set of internal controls of an organization, and internal controls are actions or procedures to ensure that activities are taking place according to planning.

In turn, it is up to the internal audit to evaluate the proper functioning of internal controls. In this wake, Filho (2008) highlights the role of internal audit in the evaluation of internal controls:

A diferença conceitual entre Sistema de Controle Interno, Controle Interno e Auditoria Interna resume-se no seguinte: Sistema é o funcionamento integrado dos Controles Internos; Controle Interno é o conjunto de meios de que se utiliza uma entidade pública para verificar se suas atividades estão se desencadeando como foram planejadas; e Auditoria Interna é uma técnica utilizada para checar a eficiência do Controle Interno (FILHO, 2008, p. 201).

Regarding international standards on the role of internal audit in the internal control system, the Institute of Internal Auditors – IIA (2009, p. 1) published the positioning statement called “O papel da auditoria interna no gerenciamento de riscos corporativo”, dealing with the activities that can be assumed by the internal audit.

In addition, the IIA positioning statement (2013, p.1) entitled “As três linhas de defesa no gerenciamento eficaz de riscos e controles” established the role of internal audit within the three-line defense model. The model was updated in 2020, and was called the “Modelo das três linhas do IIA 2020” (IIA, 2020, p.1). According to the current model, the role of internal auditisto provide “independent and objective evaluation and advice on the adequacy and effectiveness of governance and risk management” (IIA, 2020, p. 3).

Once the concepts about the internal control system and the role of internal audits are presented, we will deal with the internal control system and the role of the internal government audit in the public administration of the Brazilian Federal Executive Power.

2.1 THE INTERNAL CONTROL SYSTEM ACCORDING TO BRAZILIAN LEGISLATION

In the following items, we will conceptualize the internal control system, according to the dictates of the legislation in force, namely the Brazilian Federal Constitution of 1988 (BRASIL, 1988), Law 4,320/64 (BRASIL, 1964), Decree Law 200/67 (BRASIL, 1967), Law 10,180/01 (BRASIL, 2001), Decree No. 3,591/2000 (BRASIL, 2000), The Normative Instruction of the CGU No. 03/2017 (BRASIL, 2017a) and the Normative Instruction of the CGU No. 08/2017 (BRASIL, 2017b).

2.1.1 THE INTERNAL CONTROL SYSTEM ACCORDING TO THE FEDERAL CONSTITUTION, LAW 4.320/64 AND DECREE LAW 200/67

The internal control system in the Brazilian public administration was positive in the Federal Constitution of 1988, through articles 31, 70 and 74. In the case of municipalities, Article 31 establishes that the internal control system will exercise the supervision of the municipality, in the following terms:

Art. 31. A fiscalização do Município será exercida pelo Poder Legislativo Municipal, mediante controle externo, e pelos sistemas de controle interno do Poder Executivo Municipal, na forma da lei (grifos nossos).

§1º O controle externo da Câmara Municipal será exercido com o auxílio dos Tribunais de Contas dos Estados ou do Município ou dos Conselhos ou Tribunais de Contas dos Municípios, onde houver (BRASIL, 1988).

In the case of the Union, the supervision will take place in a broad spectrum of activities, covering operations, assets, finances and budget, both by the internal control system of the Executive, Legislative and Judicial Branches, as well as by external control, which is exercised by the Legislative Power in the three powers, with the help of the Court of Auditors:

Art. 70. A fiscalização contábil, financeira, orçamentária, operacional e patrimonial da União e das entidades da administração direta e indireta, quanto à legalidade, legitimidade, economicidade, aplicação das subvenções e renúncia de receitas, será exercida pelo Congresso Nacional, mediante controle externo, e pelo sistema de controle interno de cada Poder. (BRASIL, 1988, grifos nossos)

It should be emphasized that, in the case of the Legislative Power, the system of internal and external control exist within the same Power, the first being exercised in the administrative function and the second in the scope of their houses (House of Representatives and Federal Senate). In fact, each Power shall maintain an integrated internal control system to evaluate the execution of budgets directly or by transfers of resources to other entities, compliance and management results, in addition to the control of credit operations, guarantees and guarantees, as provided for in Article 74:

Art. 74. Os Poderes Legislativo, Executivo e Judiciário manterão, de forma integrada, sistema de controle interno com a finalidade de:

I – Avaliar o cumprimento das metas previstas no plano plurianual, a execução dos programas de governo e dos orçamentos da União;

II – Comprovar a legalidade e avaliar os resultados, quanto à eficácia e eficiência, da gestão orçamentária, financeira e patrimonial nos órgãos e entidades da administração federal, bem como da aplicação de recursos públicos por entidades de direito privado;

III – Exercer o controle das operações de crédito, avais e garantias, bem como dos direitos e haveres da União;

IV – Apoiar o controle externo no exercício de sua missão institucional.

§1º Os responsáveis pelo controle interno, ao tomarem conhecimento de qualquer irregularidade ou ilegalidade, dela darão ciência ao Tribunal de Contas da União, sob pena de responsabilidade solidária. (BRASIL, 1988, grifos nossos)

According to Law 4.320/64, internal control was related, in Article 76, to the Executive Branch, and the verification of the legality of the acts, in accordance with Article 77, may be prior, concomitant and subsequent (BRASIL, 1964). In turn, Decree Law 200/67 does not refer to the expression “internal control”, dealing only with “control”, which, according to Article 13, at the federal level, “must be exercised at all levels and in all organs” (BRASIL, 1967). The control, by Decree Law 200/67 may also be exercised by ministerial supervision, according to Article 20 and 21, which can count on the support of the central bodies, which cover financial control, in Article 22 and of a General Inspectorate of Finance in each ministry, in Article 23, item II. In indirect administration, in accordance with Article 26, sole paragraph, item “b”, ministerial supervision is exercised with the designation, by the Minister, of representatives in the control bodies (BRASIL, 1967).

It should be noted that the Constitutional Reform Proposal No. 45, of 2009, which would add item XXIII to art. 37 of the Federal Constitution of Brazil, which provides for the activities of the internal control system and includes the functions of ombudsman, inspection, government audit and correction, carried out by permanent bodies, if filed, according to consultation carried out on the website of the Federation Senate[2].

2.1.2 THE INTERNAL CONTROL SYSTEM ACCORDING TO LAW 10.180/2001, DECREE No. 3,591/2000, IN CGU N° 03/2017 E IN CGU N° 08/2017

The internal control system, as described in the Brazilian Federal Constitution of 1988, was initially regulated by Provisional Measure No. 480 of April 27, 1994[3], which organizes and disciplines the internal control and planning and budget systems of the executive branch and provides other measures. It was reissued numerous times from 1994 to 2001, and finally converted into Law No. 10,180/2001, which defined, in article 22, the Secretariat of Internal Control – SFC of the Compttorio General of the Union – CGU as the central body of the internal control system, whose techniques cover government audit activity and supervision (BRASIL, 2001). It is worth mentioning that the internal governmental audit activity of the CGU is carried out by the Federal Secretariat of Internal Control – SFC, located in Brasilia, as well as by the Regional Units of the CGU in all states of the Brazilian federation, comprising the activities of evaluating the achievement of the goals provided for in the multiannual plan, the implementation of government programs and budgets of the Union, as well as the evaluation of the management of federal public administrators (BRASIL, 2001).

In addition to the SFC (which carries out the internal audit activity of the central body) and the Regional Units of the CGU, the internal control system includes the sectoral bodies, such as the internal control bodies of the Ministry of Foreign Affairs, the Ministry of Defense, the Federal Attorney General’s Office and the Civil House. It is noteworthy that the Internal Government Audit Units – UAIGS were not mentioned in the internal control system of Law 10.180/01, and the fifth paragraph establishes that “sectoral agencies are subject to normative guidance and technical supervision of the central body of the System”, with no mention of the UAIGs (BRASIL, 2001).

Thus, in addition to the SFC/CGU and Regional, the Internal Control System of the Brazilian Federal Executive Power is composed of the Secretariats of Internal Control – CISETs of the Presidency of the Republic, the Attorney General of the Union, the Ministry of Foreign Affairs, the Ministry of Defense and their respective sectoral Units. Article 15 of Decree No. 3,591/2000 included the Internal Audits of indirect administration in the scope of the SFC/CGU, as follows:

Art. 15. As unidades de auditoria interna das entidades da Administração Pública Federal indireta vinculadas aos Ministérios e aos órgãos da Presidência da República ficam sujeitas à orientação normativa e supervisão técnica do Órgão Central e dos órgãos setoriais do Sistema de Controle Interno do Poder Executivo Federal, em suas respectivas áreas de jurisdição (BRASIL, 2000).

Therefore, according to Decree 3.591/2000, which was published even before Law 10,180/2001, it is up to the CGU and the CISETs to exercise technical supervision and normative guidance of internal audits of indirect administration (BRASIL, 2000).

The Normative Instruction CGU No. 03/2017, in addition to recognizing that the model of the three lines or layers of defense were already defined since Decree Law No. 200/1967, highlights that internal control is applied at all levels and in all organs and entities, in the following terms:

As diretrizes para o exercício do controle no âmbito do Poder Executivo Federal (PEF) remontam à edição do Decreto-Lei nº 200, de 25 de fevereiro de 1967, que, ao defini-lo como princípio fundamental para o exercício de todas as atividades da Administração Federal, aplicado em todos os níveis e em todos os órgãos e entidades, segmentou-o em três linhas (ou camadas) básicas de atuação na busca pela aplicação eficiente, eficaz e efetiva dos recursos. Como consequência, verifica-se que o controle é exercido em diversos ambientes normativos e culturais, quais sejam: a gestão operacional; a supervisão e o monitoramento; e a auditoria interna (BRASIL, 2017a).

Thus, IN CGU No. 03/2017 highlights that the internal control system is applicable at all levels and in all entities and is related to the model of the three lines, since 1967. However, under Law No. 10,180/2001, IN CGU No. 03/2017 reproduced the provisions relating to the Internal Control System, in order to structure it with the SFC/CGU occupying the position of central organ of the system and having as sectoral bodies the CISETs. In turn, individual internal audits of the organs and entities of the Federal Executive Power (Audin) and the National Audit Department of the Unified Health System – Denasus of the Ministry of Health were defined as auxiliary bodies to SCI (BRASIL, 2017a).

The Manual of technical guidance of the internal government audit activity of the Federal Executive Power, published through Normative Instruction CGU No. 08/2017, was intended to

a orientar tecnicamente os órgãos e unidades que integram o Sistema de Controle Interno do Poder Executivo Federal (SCI) e as auditorias internas singulares dos órgãos e entidades do Poder Executivo Federal (Audin) sobre os meios de operacionalizar os conteúdos constantes do Referencial Técnico (BRASIL, 2017b).

The Manual describes and disciplines the audit, consulting and verification activities for the Internal Government Audit Units – UAIG within the scope of the SCI, defining that the UAIG are “the member units of the SCI and the auxiliary bodies”. Thus, the UAIG “are positioned in the third line of defense of the Federal Executive Power”. In addition, the Manual highlights that

a contratação de empresas privadas para a atividade de auditoria interna governamental deve ser admitida somente quando verificada a impossibilidade de execução dos trabalhos de auditoria diretamente pela SFC/CGU ou órgãos setoriais (CGU, 2017b).

As established in Decree Law No. 200/1967 and IN CGU No. 03/2017, internal control is structured according to the model of the three lines. In this way, we will address, within the federal executive branch, the model in question and define the roles of management and internal government audit.

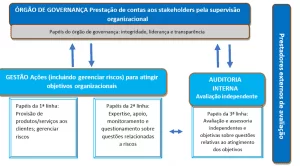

2.2 THE MODEL OF THE 3 LINES IN FEDERAL LEGISLATION

The model of the three lines of the IIA (2020) is present in the Brazilian legal system through provisions of Decree Law 200/1967, of Normative Instruction MP/CGU No. 01/2016, IN CGU No. 03/2017, IN CGU No. 08/2017 and Law 14.133/2021.

For Decree-Law No. 200/67, the control function must be exercised in a decentralized manner, in accordance with Articles 10 and 13. The internal control system is exercised in three layers, starting with federal agencies, which are responsible for the execution itself, thus regulating the first line of defense. In the second line of defense, we have the specialized bodies and in the third line, the audit. As we can understand, this model was edited long before the advent of the IIA’s three-line defense model in 2013.

This model is highlighted in Article 13 of Decree Law No. 200/67, in the following terms:

Art. 13 O controle das atividades da Administração Federal deverá exercer-se em todos os níveis e em todos os órgãos, compreendendo, particularmente:

O controle, pela chefia competente, da execução dos programas e da observância das normas que governam a atividade específica do órgão controlado;

O controle, pelos órgãos próprios de cada sistema, da observância das normas gerais que regulam o exercício das atividades auxiliares;

O controle da aplicação dos dinheiros públicos e da guarda dos bens da União pelos órgãos próprios do sistema de contabilidade e auditoria (BRASIL, 1967).

Thus, it was already defined in Decree Law No. 200/67, through items “a”, “b” and “c”, which would later be called the model of the three lines of defense, also dealing with the cost-benefit ratio between internal controls and inherent and residual risks, according to Article 14: “Administrative work will be rationalized by simplifying processes and suppressing controls that are evidenced as purely formal or whose cost is of course higher than the risk” (BRASIL, 1967).

Normative Instruction MP/CGU No. 01/2016 adopted the three-line model with the internal audit occupying the third line. In Article 2, item III, it is stated that the internal audit is an independent and objective activity of evaluation and consulting, so that they (internal audits within the public administration) constitute the third line of organizations (BRASIL, 2016a).

IN CGU No. 03/2017 has made it available that the internal controls structure follows the model of the three lines of defense, with internal audit activity occupying the third line and that “within the framework of the third line of defense, SFC and CISET perform the function of internal governmental audit in a concurrent and integrated way with audin, where they exist” (CGU, 2017).

In the Manual of technical guidance of the internal governmental audit activity of the Federal Executive Power (IN CGU No. 08/2017), all UAIG, including the SFC/CGU, CISET and individual audits, are organs of the third line of defense. For example, in item 1.2, item “b”, it is foreseen that any UAIG may “assist the organs and entities of the Federal Executive Power in structuring and strengthening the first and second lines of defense of management” (CGU, 2017).

In turn, the new Bidding Law, Law 14.133/2021, defined the three lines as follows:

Art. 169. As contratações públicas deverão submeter-se a práticas contínuas e permanentes de gestão de riscos e de controle preventivo, inclusive mediante adoção de recursos de tecnologia da informação, e, além de estar subordinadas ao controle social, sujeitar-se-ão às seguintes linhas de defesa:

I – Primeira linha de defesa, integrada por servidores e empregados públicos, agentes de licitação e autoridades que atuam na estrutura de governança do órgão ou entidade;

II – Segunda linha de defesa, integrada pelas unidades de assessoramento jurídico e de controle interno do próprio órgão ou entidade;

III – Terceira linha de defesa, integrada pelo órgão central de controle interno da Administração e pelo tribunal de contas (BRASIL, 2021b).

In this law, the audit function was not limited to the internal government audit, but covered the external control exercised by the courts of accounts of all spheres. It is worth noting that placing external control in the third line of defense is not foreseen in the three-line model, which considers only internal audit as the third line.

In the context of Brazilian federal law, due to the conceptual error of article 169 item III in relation to the model of the three lines of the IIA, this item of the new bidding law is in line with Article 13 of Decree Law No. 200/67, Article 2 of IN MP/CGU No. 01/2016 and IN CGU No. 08/2017. However, because it does not deal exclusively with internal or external control, Article 169 does not conflict with CFb/88, which establishes, in Article 74, that the internal control system will provide support to internal control in the exercise of its institutional mission. Within the states, Federal District and municipalities, it will be necessary to analyze the legislation to verify if there is conflict with item III of Article 169 of the new Bidding Law. For the direct, local and foundational administration of the Union, we will analyze and discuss this and other provisions that deal with the control in the Bidding Law in the following items.

2.3 AUDIT AND CONTROL: SIMILARITIES AND DIFFERENCES

The internal governmental audit, according to Law 10.180/2001, is carried out through the SFC/CGU and CISET, and Decree 3,591/2000 includes internal audits as auxiliary bodies of the Internal Control System of the Federal Executive Power (BRASIL, 2000). For IN MP/CGU n° 01/2016 (BRASIL, 2016a), the government internal audit activity is carried out by the aforementioned agencies, in the role of third line of defense, understanding aligned with IN CGU n° 03/2017 (CGU, 2017a) and IN CGU n° 08/2017 (CGU, 2017b). Law 13.303/2016 deals with the activity of internal audit in Articles 9, item III and § 3, in addition to Article 24, item III and VI (BRASIL, 2016b).

Law No. 14,129/2021, which provides for principles, rules and instruments for the Digital Government and for increasing public efficiency, defined the internal audit activity in article 49, namely:

Art. 49. A auditoria interna governamental deverá adicionar valor e melhorar as operações das organizações para o alcance de seus objetivos, mediante a abordagem sistemática e disciplinada para avaliar e melhorar a eficácia dos processos de governança, de gestão de riscos e de controle, por meio da:

I – Realização de trabalhos de avaliação e consultoria de forma independente, conforme os padrões de auditoria e de ética profissional reconhecidos internacionalmente;

II – Adoção de abordagem baseada em risco para o planejamento de suas atividades e para a definição do escopo, da natureza, da época e da extensão dos procedimentos de auditoria;

III – Promoção da prevenção, da detecção e da investigação de fraudes praticadas por agentes públicos ou privados na utilização de recursos públicos federais (BRASIL, 2021a).

As we have seen earlier, the SCI, as with Articles 70 and 74 of the CFb/88 and Decree Law 200/1964, is an integrated system, within each Power and adherent to the model of the three lines of defense, as we saw in IN MP/CGU no. 01/2016, IN CGU no. 03/2017 and IN CGU no. 08/2017.

The external audit is carried out in the Union, through the Federal Court of Auditors, within the scope of external control, control that provided for in Article 71 of the CFb/88. These audits of the TCU are provided for in Law No. 8,443/1992, in various provisions (BRASIL, 1992). Within the other federative entities, external control and auditing are exercised by the respective courts of accounts, through their own regulations.

According to the IIA’s positioning statements regarding the three-line model and the role of internal auditing, the role of internal audit ing is within the entity’s internal control system, but differs from the role of management, as it is in the third line (IIA, 2020). For example, according to the IIA (2009), it is not the role of the internal audit to be responsible for the organization’s internal control system. According to COSO (2013), it is not up to the internal audit to decide on which internal controls should or should not be implemented, nor the definition of risk appetite.

Therefore, for the IIA, the internal audit is a subset of the internal control system, which consists of both the first and second lines (management) and the third line (internal audit) whose role is evaluation and consulting (IIA, 2020). COSO (2013) does not provide a definition of what the internal control system is, but uses this expression multiple times in a context of an entity as a whole, as the sum of all internal controls of an organization.

Although the IIA and COSO make it clear that the concepts of internal control system and internal audit refer to different meanings, Law 10.180/2001 and Decree 3.591/2000 use the term “Internal Control System” to designate a group of internal government audit bodies, such as the SFC/CGU and CISETs, referring to them as control bodies and not only as audit units. As if that were not enough, the new Bidding Law, in several points, refers to the term “internal control” both in relation to internal control of management and to internal control related to audit activity, such as Articles 8, § 3 and Article 19, item IV dealing with the second line and Article 141, §§ 1 and 2, dealing with the third line and the court of auditors. In Article 169, the term “internal control” refers to the internal audit body of the person, with both internal and external control in the same line of defense, by including the court of auditors in the third line (BRASIL, 2021b).

2.3.1 THE INTERNAL CONTROL SYSTEM AND AUDIT IN LAW 10.180/2001

As we have seen, Article 22 of Law 10.180/2001 treats as the “Internal Control System”, the SFC/CGU as the central body and the CISET as sectoral bodies. In relation to these definitions, the TCU, in 2009, through the publication entitled “Critérios Gerais de Controle Interno na Administração Pública: um estudo dos modelos e das normas disciplinadoras em diversos países” defines the internal control system as a set of activities, a process of responsibility of management, to give reasonable assurance that the objectives will be achieved (TCU, 2009).

In fact, the TCU defined the internal control, system or internal control structure as:

expressões sinônimas, utilizadas para referir-se ao processo composto pelas regras de estrutura organizacional e pelo conjunto de políticas e procedimentos adotados por uma organização para a vigilância, fiscalização e verificação, que permite prever, observar, dirigir ou governar os eventos que possam impactar na consecução de seus objetivos (TCU, 2009, p. 4).

In addition, the “internal control unit, when existing in the organization, is part of the management and the internal control system or structure of the entity itself” (TCU, 2009, p. 6), while the “internal audit, which should not be confused with internal control or with internal control unit, (…) its task is to measure and evaluate the efficiency and effectiveness of other controls” (TCU, 2009, p.7).

According to the TCU Survey Report, published in 2017 (TC 011.759/2016-0) internal control is “an action, an activity, a procedure” and responsibility of management (BRASIL, 2017, p. 7). In addition, according to the TCU “The internal control system of an organization is formed by the three lines of defense”, with the internal audit as the third line (BRASIL, 2017, p. 8). Later, citing Decree 3.591/2000, the TCU points out that “in Brazil there is no clear use of these concepts and the legislation itself is confusing” (BRASIL, 2017, p. 11).

Following the line of reasoning, the TCU highlights, among some problems of confusion between the concepts, that “it does not make sense to use the expression ‘internal control body'” and that this expression “may cause the manager not to feel responsible for the establishment of internal controls, because, in his view, there is an internal control body just to do this” (BRASIL, 2017, p. 16).

Therefore, these conceptual inaccuracies of Law No. 10,180/2001 and Decree No. 3,591/2000 are reproduced in other legal provisions, in which it treats the SFC/CGU, CISETs and individual internal audits simply as “internal control bodies” or as “organs that are part of the internal control system”, such as Decree 7.768/2011, art. 7, Decree 2.451/1998, art. 22, Decree 7.689/2012, art. 8, Decree 6.932/2009, Art. 17 (TCU, 2009, p. 17).

Similarly, such confusion between internal control concepts and internal audit seems to have also occurred in the new Bidding Law, which we will analyze below.

2.3.2 INTERNAL CONTROL AND INTERNAL AUDIT IN LAW No. 14.133/2021

To understand the purposes of the new bidding law, we will cite Article 181 of Chapter III, which deals with the transitional and final provisions:

Art. 181. Os entes federativos instituirão centrais de compras, com o objetivo de realizar compras em grande escala, para atender a diversos órgãos e entidades sob sua competência e atingir as finalidades desta Lei.

Parágrafo único. No caso dos Municípios com até 10.000 (dez mil) habitantes, serão preferencialmente constituídos consórcios públicos para a realização das atividades previstas no caput deste artigo, nos termos da Lei nº 11.107, de 6 de abril de 2005 (BRASIL, 2021b).

In fact, one of the strategies established in the law for the better management of government procurement is the centralization of purchases for each member of the federation (BRASIL, 2021b). It should be highlighted that the law has not set a deadline for this to happen, and the Union should centralize all its purchases in a single purchasing center, which may occur within the current Ministry of Economy.

Thus, through this perspective of centralized purchases in the Union, states, Federal District and municipalities, we can better understand the purposes of the three lines of defense established through Article 169 of the Bidding Law:

Art. 169. As contratações públicas deverão submeter-se a práticas contínuas e permanentes de gestão de riscos e de controle preventivo, inclusive mediante adoção de recursos de tecnologia da informação, e, além de estar subordinadas ao controle social, sujeitar-se-ão às seguintes linhas de defesa:

I – Primeira linha de defesa, integrada por servidores e empregados públicos, agentes de licitação e autoridades que atuam na estrutura de governança do órgão ou entidade;

II – Segunda linha de defesa, integrada pelas unidades de assessoramento jurídico e de controle interno do próprio órgão ou entidade;

III – terceira linha de defesa, integrada pelo órgão central de controle interno da Administração e pelo tribunal de contas (BRASIL, 2021b).

In view of this perspective, the third line of defense would be, within the scope of internal control, the SFC/CGU itself, as the central organ of the internal control system of the Federal Executive Power, competing with CISET and internal audits in their respective areas of attributions defined in Law No. 10,180/2001 (BRASIL, 2001).

Despite the conceptual improperty of the position of the court of auditors as a third line, since it should make up a fourth line, the device is not conflicting with the CFb/88, considering that article 169 does not deal only with internal control (BRASIL, 1988).

Next, we will discuss the articles of law that deal with control, in order to establish the competencies of management and internal audit.

In Article 8, § 3, the law on bids states that:

Art. 8º A licitação será conduzida por agente de contratação, pessoa designada pela autoridade competente, entre servidores efetivos ou empregados públicos dos quadros permanentes da Administração Pública, para tomar decisões, acompanhar o trâmite da licitação, dar impulso ao procedimento licitatório e executar quaisquer outras atividades necessárias ao bom andamento do certame até a homologação.

(…)

§3º As regras relativas à atuação do agente de contratação e da equipe de apoio, ao funcionamento da comissão de contratação e à atuação de fiscais e gestores de contratos de que trata esta Lei serão estabelecidas em regulamento, e deverá ser prevista a possibilidade de eles contarem com o apoio dos órgãos de assessoramento jurídico e de controle interno para o desempenho das funções essenciais à execução do disposto nesta Lei (BRASIL, 2021b).

In the case of § 3 of Article 8 of the Law, the function of advising can be done both by the specialized bodies of the second line (management) and by the third line (UAIG). In the case of providing advisory and consulting services, IN CGU no. 08/2017 (BRASIL, 2017b) highlights this type of activity, noting that the IIA’s positioning statement for the role of internal audit also highlights the safeguards to be adopted by internal audits.

Regarding the implementation of preventive internal controls by management, Article 19, VI establishes the following:

Art. 19. Os órgãos da Administração com competências regulamentares relativas às atividades de administração de materiais, de obras e serviços e de licitações e contratos deverão:

(…)

IV – Instituir, com auxílio dos órgãos de assessoramento jurídico e de controle interno, modelos de minutas de editais, de termos de referência, de contratos padronizados e de outros documentos, admitida a adoção das minutas do Poder Executivo federal por todos os entes federativos (BRASIL, 2021b);

In relation to Article 19, IV, we understand the institution of these document models is not the role of internal audit (UAIG), considering that the statement of positioning on the role of internal audit in risk management (IIA, 2009), indicates that decision-making and implementation of risk responses should not be a role that the internal audit should assume. Similarly, COSO (2013) establishes that it is the role of management to take responses to risks or internal management controls. However, UAIG, within the scope of the consultancy, will be able to assist the other lines in the elaboration of these models, with the necessary safeguards related to the management’s own attributions.

In the stage of information and communication of any change in the chronological order of payments to suppliers of goods and/or services, Article 141, §§ 1 and 2 provides that:

Art. 141. No dever de pagamento pela Administração, será observada a ordem cronológica para cada fonte diferenciada de recursos, subdividida nas seguintes categorias de contratos:

(…)

§1º A ordem cronológica referida no caput deste artigo poderá ser alterada, mediante prévia justificativa da autoridade competente e posterior comunicação ao órgão de controle interno da Administração e ao tribunal de contas competente

(…)

§2º A inobservância imotivada da ordem cronológica referida no caput deste artigo ensejará a apuração de responsabilidade do agente responsável, cabendo aos órgãos de controle a sua fiscalização (BRASIL, 2021b).

In this provision, for the case of internal control, we understand that the communication should be forwarded to the SFC/CGU or CISET and to the internal audit of the unit, in case there is an internal audit unit in the organization framed in Article 141, § 1 (BRASIL, 2021b).

Thus, we understand that internal audits act in the third line (defense), and that they were not mentioned directly in the text probably because the third line is centralized in the central organ of the internal control system in each dimension of the federation. Therefore, the purpose of the law, when establishing a purchasing center in each entity of the federation, is to consider that the third line would be centralized in the central internal control body of each entity, with the first and second lines within the respective entity.

Internal audits, although located within each organization, by the normative framework and IIA positioning statements are always in the third line, providing evaluation and consulting to their respective organizations. In turn, the central internal audit body provides evaluation and consulting within its respective federative entity, acting in a concurrent manner with the internal audits of each entity with its own legal personality.

3. METHODOLOGY

In order to provide the achievement of the proposed results, on the basis of consistent argumentation, this article used as a basis a descriptive research, which, according to Silva (2003), is the one that aims to identify the characteristics of the phenomenon under analysis and establish relationships between the variables. Thus, data collection was performed through a literature review, with the knowledge of the IIA positioning statements, COSO (2013) provisions, as well as the current regulations.

The legal diplomas were selected from research on official sites, such as those of the CGU and the Civil House of the Presidency of the Republic and submitted to a content analysis, which, according to Bardin (1977), covers the reading of all material, with the selection of words and sets of words that make sense, followed by the classification of these words or phrases into categories or themes.

Thus, the information was treated in a qualitative analysis, which, for Gil (2008, p. 175), is used for experimental research, when “there are no predefined formulas or recipes to guide researchers”. Therefore, the bibliographic research allowed the discussion of the results and conclusion about the roles played by the internal government audit in the context of the new bidding law, in order to ensure the correct segregation of functions and preservation of the independence of the third-line body.

4. RESULTS AND DISCUSSION

Since we conceptualize the internal control system according to Brazilian legislation, with a fulcrum in the Brazilian Federal Constitution and other legal provisions, addressing the model of the 3 lines of the Institute of Internal Auditors – IIA (2020) and its effects on federal legislation, considering that we deal with the similarities and differences of audit and control, we will be able to interpret the provisions of the new bidding law in line with the Federal Constitution (BRASIL,1988) and current legal norms, in order to delimit the role of internal government audit in the internal control system, at the federal level.

Indeed, if we adopt a technique of legal hermeneutics (ÂMBITO JURÍDICO, 2019), for the interpretation of the new Law 14.133/2021 and Law 10.180/2001, systematically with other legal provisions (LEITE, 2020), because of the vague or ambiguous meaning of the expressions “control”, “internal control” or “internal control system”, we must also verify which activity in question, whether it is government management or internal audit. Thus, for the analysis of the devices, we must take into account both the international standards and standards of internal audit, risk management and internal control and the normative basis related to the theme, namely CFb/88, Decree Law No. 200/1967, IN MP/CGU no. 01/2016, IN CGU no. 03/2017 and IN CGU No. 08/2017.

On the other hand, we should not interpret the bidding law solely on the basis of the expression “internal control” without considering the context of the framework of the activity in internal audit (third line) or management (first and second lines). For this framework, as we said, we should consult international standards and applicable regulatory basis.

Furthermore, considering the provisions of Article 15 of Decree 3.591/2000 and in order to make Law 10,180/2001 compatible with the Brazilian Federal Constitution, in the sense that internal audits also perform the function of government audit, in accordance with Articles 70 and 74 of the CFb/88, we must interpret Law 10.180/2001 and Decree No. 3,591/2000 in order to understand that the relationship of organs that are part of the internal control system is an example of and that the expression “internal control” corresponds to the audit activity, according to the caput of Article 21 of Law 10.180/2001. This interpretation is possible through the use of the word “integrate”, understood as inclusion to a larger set and not as an exhaustive enumeration[4]. On the other hand, legal provisions should not be interpreted as an exhaustive enumeration, meaning that the internal control system is the sole and exclusive competence of the internal governmental audit bodies related to these regulations.

Due to the information presented, we can identify which control body is responsible for acting at each mention in the legal text, both in the second line and in the third line, as we will see below.

In Article 169, item III of Law No. 14.133/2021, the body, at the federal level, is the SFC/CGU, in the case of acquisitions made centrally, in accordance with Article 181 and, within the scope of each law ing body, ciset and UAIG, which are in a concurrent and integrated manner with the CGU.

In the case of § 3 of Article 8 of this law, the function of advisory can be done both by the specialized bodies of the second line (bodies that act in the management of the governmental entity) and by the third line (UAIG), with the appropriate safeguards.

In relation to Article 19, IV, the organs “of the Administration with regulatory powers relating to the activities of materials management, works and services and tenders and contracts shall” (…) “institute … models of draft notices, terms of reference, standardized contracts and other documents” are the second-line bodies, and the UAIG is responsible for assisting in the preparation of these documents in the form of consulting and advisory, with the necessary safeguards.

Finally, the justification for the change of the chronological order of payment, according to Article 141, § 1, should be made to the SFC/CGU or CISET and to the internal audit of the unit, if any, as an internal control body in the third line, together with the communication to the TCU.

Therefore, the role of the singular internal audit units (UAIG) of the federal public administration, in relation to Law No. 14,133/2021, is that of evaluation and consulting in their respective organizations, in a manner concurrent to the central body of the internal control system and sectoral agencies, as the case may be.

5. CONCLUSION

The definition of the role of internal audit and individual audits in the municipal and foundational entities of the Federal Executive Power, both within the scope of the new bidding law and in other contexts, is of central importance for compliance with the legislation and for the effective functioning of the internal control system, due to the large number of entities of indirect administration and the materiality of federal resources subject to evaluation.

In this sense, we conceptualized the internal control system, based on the Federal Constitution and other legal norms, in accordance with the model of the 3 lines of the Institute of Internal Auditors – IIA (2020) and other applicable international standards, to address the similarities and differences between audit and control. Next, we interpret the articles of the new bidding law that mention the control to delimit the role of internal government audit in the internal control system, in line with the Federal Constitution and current legal norms.

Therefore, when identifying the different actors that are members of the SCI, in comparison with the current legislation, we understand that the role of the UAIG of the indirect federal public administration, in view of Law No. 14,133/2021, is the third line or layer, performing the activity of internal governmental audit, which is composed of evaluation and consulting, acting within the scope of their respective entities, independently and concurrent to the central body of the internal control system and sectoral bodies, as we saw earlier.

Given that the theme is recent, given the beginning of the validity of the new bidding law, it is understood that the theme in question can subsidize future regulation of its devices, besides being subject to the agenda, to be taken to the Internal Control Coordination Commission (CCCI), a collegiate body of the CGU, of consultative function for this, in the use of the competencies set out in Art. 10 of Decree No. 3,591/2000, in particular item II, decide on the interpretations to be signed for the federally in force basis, namely Law 14.133/20121, in order to delimit the role of the agents responsible for each line (or layer) and who integrate the internal control structure of the organs and entities of the Federal Executive Power.

REFERENCES

ÂMBITO JURÍDICO, 2019. Disponível em: https://ambitojuridico.com.br/cadernos/direito-civil/a-hermeneutica-juridica-parte-1-sistemas-e-meios-intrepretativos/#:~:text=O%20objeto%20da%20hermen%C3%AAutica%20%C3%A9,o%20sentido%20da%20norma%20jur%C3%ADdica. Acesso em: 04 ago. 2021.

BARDIN, L. Análise de conteúdo. Lisboa: Edições 70, 1977.

BRASIL. Constituição da república federativa do Brasil, 1988. Brasília, 1988. Disponível em: http://www.planalto.gov.br/ccivil_03/constituicao/constituicao.htm. Acesso em: 04 ago. 2021.

________. Controladoria-Geral da União. Instrução Normativa Conjunta nº 1, de 10 de maio de 2016. Dispõe sobre controles internos, gestão de riscos e governança no âmbito do Poder Executivo federal. Brasília, 2016a. Disponível em: https://www.in.gov.br/materia/-/asset_publisher/Kujrw0TZC2Mb/content/id/21519355/do1-2016-05-11-instrucao-normativa-conjunta-n-1-de-10-de-maio-de-2016-21519197. Acesso em: 04 ago. 2021.

________. Controladoria-Geral da União. Instrução Normativa nº 3, de 9 de junho de 2017. Aprova o Referencial Técnico da Atividade de Auditoria Interna Governamental do Poder Executivo Federal. Brasília, 2017a. Disponível em: https://www.in.gov.br/materia/-/asset_publisher/Kujrw0TZC2Mb/content/id/19111706/do1-2017-06-12-instrucao-normativa-n-3-de-9-de-junho-de-2017-19111304. Acesso em: 04 ago. 2021.

________. Controladoria-Geral da União. Instrução Normativa nº 8, de 6 de dezembro de 2017. Manual de Orientações Técnicas da Atividade de Auditoria Interna Governamental do Poder Executivo Federal. Brasília, 2017b. Disponível em: https://www.in.gov.br/materia/-/asset_publisher/Kujrw0TZC2Mb/content/id/1096823/do1-2017-12-18-instrucao-normativa-n-8-de-6-de-dezembro-de-2017-1096819-1096819. Acesso em: 04 ago. 2021.

_______. Decreto-Lei nº 200, de 25 de fevereiro de 1967. Dispõe sobre a organização da Administração Federal, estabelece diretrizes para a Reforma Administrativa e dá outras providências. Brasília, 1967. Disponível em: http://www.planalto.gov.br/ccivil_03/decreto-lei/del0200.htm. Acesso em: 04 ago. 2021.

________. Decreto nº 3.591, de 6 de setembro de 2000. Dispõe sobre o Sistema de Controle Interno do Poder Executivo Federal e dá outras providências. Brasília, 2000. Disponível em: http://www.planalto.gov.br/ccivil_03/decreto/D3591.htm. Acesso em 19/05/2019.

_______. Lei n° 4.320, de 17 de março de 1964. Estatui Normas Gerais de Direito Financeiro para elaboração e controle dos orçamentos e balanços da União, dos Estados, dos Municípios e do Distrito Federal. Brasília, 1964. Disponível em: http://www.planalto.gov.br/ccivil_03/leis/l4320.htm. Acesso em: 04 ago. 2021.

_______. Lei Nº 8.443, de 16 de julho de 1992. Dispõe sobre a Lei Orgânica do Tribunal de Contas da União e dá outras providências. Brasília, 1992. Disponível em: http://www.planalto.gov.br/ccivil_03/leis/l8443.htm. Acesso em: 05 ago. 2021.

_______. Lei n° 10.180, de 6 de fevereiro de 2001. Organiza e disciplina os Sistemas de Planejamento e de Orçamento Federal, de Administração Financeira Federal, de Contabilidade Federal e de Controle Interno do Poder Executivo Federal, e dá outras providências. Brasília, 2001. Disponível em: Disponível em: http://www.planalto.gov.br/ccivil_03/LEIS/LEIS_2001/L10180.htm. Acesso em: 04 ago. 2021.

________. Lei Nº 13.303, de 30 de junho de 2016. Dispõe sobre o estatuto jurídico da empresa pública, da sociedade de economia mista e de suas subsidiárias, no âmbito da União, dos Estados, do Distrito Federal e dos Municípios. Brasília, 2016b. Disponível em: http://www.planalto.gov.br/ccivil_03/_ato2015-2018/2016/lei/l13303.htm. Acesso em: 04 ago. 2021.

________. Lei nº 14.129, de 29 de março de 2021. Dispõe sobre princípios, regras e instrumentos para o Governo Digital e para o aumento da eficiência pública e altera a Lei nº 7.116, de 29 de agosto de 1983, a Lei nº 12.527, de 18 de novembro de 2011 (Lei de Acesso à Informação), a Lei nº 12.682, de 9 de julho de 2012, e a Lei nº 13.460, de 26 de junho de 2017. Brasília, 2021a. Disponível em: https://www.in.gov.br/en/web/dou/-/lei-n-14.129-de-29-de-marco-de-2021-311282132. Acesso em: 05 ago. 2021.

________. Lei n° 14.133, de 1° de abril de 2021. Lei de Licitações e Contratos Administrativos. Brasília, 2021b. Disponível em: https://www.in.gov.br/en/web/dou/-/lei-n-14.133-de-1-de-abril-de-2021-311876884. Brasília, 2021b. Acesso em: 04 ago. 2021.

________. Tribunal de Contas da União. Acórdão nº 1171/2017 – TCU – Plenário: Relatório de Levantamento TC 011.759/2016-0. Brasília, 2017. Disponível em: https://portal.tcu.gov.br/lumis/portal/file/fileDownload.jsp?fileId=8A8182A25EABAA93015EBEA525695384. Acesso em: 04 ago. 2021.

________. Tribunal de Contas da União. Critérios Gerais de Controle Interno na Administração Pública: um estudo dos modelos e das normas disciplinadoras em diversos países. Brasília, 2009. Disponível em: https://portal.tcu.gov.br/lumis/portal/file/fileDownload.jsp?fileId=8A8182A15A4C80AD015A4D5CA9965C37. Acesso em: 04 ago. 2021.

COSO – Committee of Sponsoring Organizations of the Treadway Commission. Controle Interno – estrutura integrada: sumário executivo. São Paulo: IIA Brasil, 2013.

COSO – Committee of Sponsoring Organizations of the Treadway Commission. Gerenciamento de riscos corporativos – estrutura integrada: sumário executivo. Jersey City, 2007. Disponível em: http:www.coso.org/documents/COSO_ERM_ExecutiveSummnary_Portuguese.pdf. Acesso em: 04 ago. 2021.

DE OLIVEIRA, Denise Fontenele. O controle interno e auditoria governamental: comparativo. Revista Controle-Doutrina e Artigos, v. 12, n. 1, p. 196-211, 2014. Disponível em: https://revistacontrole.tce.ce.gov.br/index.php/RCDA/article/download/211/213.

Instituto de Auditores Internos. Declaração de posicionamento do IIA: o papel da auditoria interna no gerenciamento de riscos corporativo. Lake Mary, Fl: The Institute of Internal Auditors, 2009. Disponível em: https://iiabrasil.org.br/korbilload/upl/ippf/downloads/declarao-de-pos-ippf-00000001-21052018101250.pdf. Acesso em 04 ago. 2021.

Instituto de Auditores Internos. Declaração de Posicionamento do IIA: O Papel da Auditoria Interna na Governança Corporativa. Lake Mary, FL: The Institute of Internal Auditors, 2018. Disponível em: https://iiabrasil.org.br/korbilload/upl/ippf/downloads/declarao-de-pos-ippf-00000006-14062018163019.pdf. Acesso em 04 ago. 2021.

Instituto de Auditores Internos. Declaração de posicionamento do IIA: as três linhas de defesa no gerenciamento eficaz de riscos e controles. Lake Mary, FL: The Institute of Internal Auditors, 2013. Disponível em: https://repositorio.cgu.gov.br/handle/1/41842. Acesso em 04 ago. 2021.

Instituto de Auditores Internos. Modelo das Três Linhas do IIA 2020: uma atualização das três linhas de defesa. Lake Mary, FL: The Institute of Internal Auditors, 2020. Disponível em: https://iiabrasil.org.br/korbilload/upl/editorHTML/uploadDireto/20200758glob-th-editorHTML-00000013-20072020131817.pdf. Acesso em 04 ago. 2021.

GIL, Antonio Carlos. Métodos e técnicas de pesquisa social. 6. ed. Editora Atlas SA, 2008.

FILHO, A. J. A importância do controle interno na administração pública. Diversa, Ano I – nº 1, p. 85-99, jan./jun, 2008. Disponível em: http://capa.tre-rs.gov.br/arquivos/JOSE_controle_interno.PDF. Acesso em: 01 jul. 2021.

MAIA, Matheus Silva et al. Contribuição do sistema de controle interno para a excelência corporativa. Revista Universo Contábil, v. 1, n. 1, p. 54-70, 2005. Disponível em: http://www.rep.educacaofiscal.com.br/100913090539auditoria_interna_e_o_controle_interno.pdf. Acesso em: 01 jul. 2021.

LEITE, Gisele. Da Hermenêutica para a compreensão da lei e do Direito. Jornal Jurid, Bauru, ago. 2020. Disponível em: https://www.jornaljurid.com.br/colunas/gisele-leite/da-hermeneutica-para-a-compreensao-da-lei-e-do-direito. Acesso em: 01 jul. 2021.

RIBEIRO, Renor Antonio Antunes. O papel da auditoria interna na gestão de riscos em entidades do setor público de Portugal e do Brasil. 2019. Dissertação de Mestrado. Disponível em: https://repositorium.sdum.uminho.pt/bitstream/1822/64581/1/Renor+Antonio+Antunes+Ribeiro.pdf. Acesso em: 01 jul. 2021.

RIBEIRO, Renor. Gestão de Riscos no Setor Público: normas e padrões internacionais, análise das legislações nacionais de Portugal e do Brasil e aplicação na base normativa do setor público. 1ª ed. Brasília: Athenas Editora, 2020a.

RIBEIRO, Renor. Gestão de Riscos em Organizações Públicas: normas e padrões internacionais utilizados para a gestão de riscos, etapas do processo e análise da base normativa de Portugal e do Brasil. 1ª ed. Lisboa: Edições Exlibris, 2020b.

SILVA, E. L.; MENEZES, E. M. Metodologia da pesquisa e elaboração de dissertação. 4. ed. rev. atual. Florianópolis: UFSC, 2005.

APPENDIX – FOOTNOTE REFERENCE

2. Available at: https://www25.senado.leg.br/web/tividade/materias/-/materia/93534

3. Available at: http://www.planalto.gov.br/ccivil_03/mpv/Antigas/480.htm#:~:text=480&text=MEDIDA%20PROVIS%C3%93RIA%20No%20480%2C%20DE%2027%20DE%20ABRIL%20DE%201994.&text=Organiza%20e%20disciplina%20os%20Sistemas,Executivo%20e%20d%C3%A1%20outras%20provid%C3%AAncias.

4. According to the Michaelis Dictionary, to integrate is: 1 Incorporating an element into a set; include, include: “The young writer won the Jabuti Prize […] and his books are also part of the basic collections of the National Foundation for Children and Youth” (TM1). Available at: https://michaelis.uol.com.br/busca?id=dNMl7#:~:text=1%20Incorporar(%2Dse)%20um,e%20Juvenil%E2%80%9D%20(%20TM1%20)%20.

[1] Master in Public Administration at Universidade do Minho – UMINHO, MBA in Strategic Management in Public Administration, Specialist in Public Administration at UMINHO, Specialist in Educational Planning, Graduated in Mechanical Engineering from UFC, Graduated in Physics from UECE, Graduated in Music Education from UnB.

Submitted: August, 2021.

Approved: September, 2021.