ORIGINAL ARTICLE

POTAS, Alberto Veiga [1]

POTAS, Alberto Veiga. Social responsibility and comparative analysis between two financial institutions. Revista Científica Multidisciplinar Núcleo do Conhecimento. Year 04, Ed. 05, Vol. 07, p. 186-209. May 2019. ISSN: 2448-0959, Access link: https://www.nucleodoconhecimento.com.br/business-administration/financial-institutions, DOI: 10.32749/nucleodoconhecimento.com.br/business-administration/financial-institutions

ABSTRACT

In this research, the theme of social responsibility aims to present and know how companies should be analyzed in the annual social balance reports. The objective is to investigate the importance and usefulness of social responsibility for companies located in Brazil, showing the actions of organizations in order to identify and verify data, information, and what projects have been carried out and existing problems. For this, it will be necessary to carry out a theoretical bibliographic research, investigating the relationship of companies with the local community, following the concept of social responsibility within ethical and moral limits. It is necessary to know which institutions carry out projects and how they are done through observations of the results, it will also be analyzed whether this procedure provides an efficient sustainable development within the region.

Keywords: Social responsibility, sustainable development, business management, sustainability, social balance.

INTRODUCTION

The work addresses a topic of great relevance in the business environment: social responsibility.

The discussion has become increasingly frequent, as it is constantly conveyed by organizations through various media, as well as in academia.

The main objective is to present the theme in a way that understands the purpose, history and concept, being able to efficiently understand the theory and application of an annual report of the social balance of two financial institutions.

Specifically, define the important elements of the theme, acquiring knowledge about the scope of social responsibility and sustainability, learn to analyze a company’s social balance and compare it with other companies with a detailed view of the analysis of the information of the results in their reports.

Chapter 1 presents the work methodology according to Severino (2007). The subject is based on exploratory and bibliographic research.

Chapter 2 introduces the subject in the study that addresses the topic in theory and history, including the technical and analytical view of the results of each institution that cares about the environment in which it relates.

Chapters 3, 4 and 5 deal with the theoretical framework that serves as the basis for the study. By uniting the concepts with the practice of defining the elements, facts, characters and main institutions, the knowledge of the theme is expanded to the history used in the analysis of other recorded works.

In chapter 6, the presentation of the companies included in this research is shown with their historical and analytical context, knowing the aspects of corporate policy of each institution and their role with social responsibility.

Chapter 7 analyzes the results of the social balance of two companies in 2013 and 2014, showing the comparison between indicators.

Finally, chapter 8 deals with the final considerations, suggesting the expansion of new research to other areas of knowledge with the help of a pedagogical approach.

METHOD

This work was based on bibliographic research in the area and theme of social responsibility and sustainability. With the speech of some authors as a reference and exploratory study, providing more information on the subject and discovering a new approach based on information from reliable sources, authors, journals and articles that helped in the construction and resolution of this work.

MILLENNIUM DEVELOPMENT GOALS (MDGs)

The United Nations (UN) promoted a debate in 2000, bringing together heads of States and Governments to establish goals throughout the 1990s, with the objective of developing means for the eradication of poverty in the world. This idea should be achieved by the year 2015.

8 objectives were created with 18 targets and 48 indicators, and these objectives should consider national specifications. Some countries are below their limit, not having the capacity to achieve means of development.

The eight objectives identified were:

1- Eradication of extreme poverty and hunger.

2- Achieve universal basic education.

3- Promotion of gender equality and women’s empowerment.

4- Reduction of infant mortality.

5- Improved maternal health.

6- Combat HIV/AIDS, malaria and other diseases.

7- Ensuring environmental sustainability.

8- Establishment of a global partnership for development.

Thus, the Millennium Development Goals (MDGs) consider the eradication of poverty, hunger and illiteracy, gender equality and environmental sustainability.

Between 1990 and 2010 extreme poverty was reduced from 47% to 22% of the world’s population, in which the target was reached. However, 1.2 billion people are still in extreme poverty in the world (earning less than US$ 1.2 a day). Access to education and health care is evolving around the world, as are environmental protection actions. In Brazil, the results of the MDGs are extremely positive, the intention is to reach or exceed these goals.

After the implementation of this idea and results, the goals were incorporated within the companies, generating a transformation in their way of managing and interacting with society.

BRIEF HISTORY OF SOCIAL RESPONSIBILITY

IN THE WORLD

In the last years of the 20th century, the consciousness of humanity brought with it new behavioral ways for society, companies and governments. Ways of thinking and acting, with globalization being accelerated. What happened brought changes with new situations and conditions to the world.

The world market has increased due to new air, sea and land transport technologies.

The means of communication and information have evolved technologically. The internet was the tool that connected and brought the world together, creating global networks and increasing the power of relationships between cultures, countries, companies and markets.

At the same time, competition between companies from different countries increased, an example of this was the competition between the United States and Japan, which gave rise to the Nylon fabric: “Now You’ve Lost, Old Nippon”.

Globalization has generated great business opportunities, on the other hand the increase in poverty and exclusion. While some countries were advanced in relation to their economy, others were marginalized. An example of this situation is in the area of education in the middle of the information age, while some countries are modernizing with computers, others suffer from the lack of conditions, for example, school materials and a well-structured place for study.

The restructuring of companies at the time led to the closing of facilities in countries with cheap labor, causing developed institutions to close activities within the communities, leaving needy countries and harming the environment with the indiscriminate use of raw material. The event contributed excessively to the overheating of the planet, pollution of rivers and seas, and the waste of garbage in large quantities.

The companies were focused only on economic and productive activities, without worrying about social and environmental impact and the development of the future.

The idea of sustainable development was enshrined in the largest meeting ever held to discuss the future of the planet, the United Nations Conference on environment and development. ECO-92, which was held in Rio de Janeiro, Martins (2011).

Novaes (1992) adds that:

“[…] pensar que o ator principal na questão das mudanças climáticas aceitasse o papel que lhe cabia — o da maior quota na redução da emissão de poluentes atmosféricos, que contribuem para o cenário em que se discutem as mudanças.” (NOVAES, 1992, pg. 80)

Sustainable development is one that generates economic knowledge, is concerned with environmental impact and is focused on community development, called the Triple Bottom Line (the union of the three p’s: People, Profit, Planet, translating people, business and planet)

To discuss the directions of globalization, governments, business sectors and NGOs met in conferences in the Social Cycle of the United Nations Organizations in the early 1990s. This meeting was held so that it was possible to review actions and create Millennium Development Goals (MDGs) , known as the millennium goals. In 2000, 191 countries committed to the targets, and in 2015, 193 countries.

IN BRAZIL

It is known for certain that the beginning of the history of social responsibility in Brazil had records in social actions of entrepreneurs since the 19th century, one can also indicate the year 1965 as one of the initial milestones of this theme. As a context, there were eminent economic gaps and the enormous delay in certain areas of the country resulting, in part, from not having the business sector fully aware of its social responsibilities, in view of this scenario, the Associação de Dirigentes Cristão de Empresas – Brasil (ADCE)[2] publishes the “Charter of Principles for Christian Business Leaders”. The document calls on the entrepreneur to understand that “business activity must not absorb the entrepreneur, nor transform the end in itself, since the company director has an obligation to participate actively and with full responsibility in the civic and political life of the community”. Freire and Silva (2001) emphasize that:

“O marco da responsabilidade social no Brasil se deu mais precisamente em 1965, com a publicação da Carta de Princípios do Dirigente Cristão de Empresas, que já nesta época, utilizava o termo responsabilidade social das empresas. Contudo, foi somente a partir dos anos 80 que pequena parcela das empresas que atuam no Brasil passara a intensificar e a institucionalizar o discurso em relação às questões sociais e ambientais, realizando também em escalas diversificadas ações sociais concretas.” (FREIRE and SILVA, 2001, pg.54)

From that point on, there was a great mobilization regarding the theme and the situation.

They created awards, debates, spaces, practices, institutes, foundations, committees and the propagation of social reports, in which today there are advanced techniques for annual sustainability reports with large numbers of pages and detailed information on company plans and actions.

In the 1980s, the first company to present its social report was Nitrofértil, in 1984, in which, without the current standardization, it was made as cordel literature.

The 1990s marked the period of emergence and consolidation of several organizations that were institutionalized to promote the issue of corporate social responsibility. This was when the idea of “corporate social responsibility” and the need to carry out and publish an annual social report in the culture of Brazilian business organizations to mature was under different national and international influences.

A very important character in this debate was Herbert José de Souza, known as Betinho, sociologist and human rights activist, responsible for founding the ADCE where the publication of the Charter of Principles of the Christian Leader of companies calls the business community to understand that the activity should not be directed towards itself, but towards community and society:

[…] deve replicar com a ação positiva e fecunda de quem oferece, em contraposição, o senso de responsabilidade dos dirigentes de empresa cônscios dos seus deveres sociais de cristãos e dispostos a lutar unidos por uma ordem social mais justa, por uma ordem econômica a serviço do homem, por um desenvolvimento integral e harmônico […] (ADCE 1967, pg.1).

With the creation of the Instituto Brasileiro de Análises Sociais e Econômicas (IBASE)[3], the importance of disclosing their social balances was transmitted, and the document was standardized for transparency and information on projects aimed at employees, investors and the community.

It is now necessary to understand that, like any other organization, companies have an evolutionary history and change relatively frequently. They work in an environment with which they relate in many ways, impacting and being impacted by everything that surrounds them, having the duty to build new actors and social scenarios integrated into society.

THE CURRENT SCENARIO OF SOCIAL RESPONSIBILITY IN BRAZIL

Brazil is the 75th country in terms of the Global HDI with 0.755 in 2014, with a population of 206,081,432 inhabitants, 47.73% white, 50.74% black and with a poverty rate of 2.8. With a territorial size of 8,514,876,599 km, representing the second largest country on the American continent, behind the United States.

According to Oliveira (2002), there is a lack of basic social services in Brazil that affects a large part of the population. The country suffers due to a series of social problems such as: income inequality, low quality of education, child labor, persistent illiteracy, one of the highest rates of accidents at work, high infant mortality in some regions, violence against women, etc. Therefore, there is a lot of room for organizations to act.

In 2001, Revista Administração revealed that more than 50% of Brazilian companies carry out some type of social action. Some social issues, such as ethnic minorities, HIV carriers, drug addicts, people with disabilities, are generally relegated to the support of a small portion of the business effort. There also seems to be a correlation between company size and volunteering, larger companies are more involved and organized of the total number of companies in Brazil, in 2004 IPEA (2006) most were located in the Southeast (48%) and in the South (30%) , with a lower participation of the Northeast (9%) and the Central-West (9%), in addition to the North (4%). In turn, the commerce (53%) and services (24%) sectors had the highest number of companies. With regard to size, it is observed that the greater the number of employees, the smaller the number of companies, that is, there are more companies in the micro category (up to 10 employees), followed by the small category (from 11 to 100 employees). ) and after the medium (101 to 500 employees) and the large (more than 500 employees), with participation 421 of 71%, 22%, 3% and 1%, respectively.

Data from IPEA (2006) indicate a significant growth (from 59% in 2000 to 69% in 2004) in the proportion of Brazilian private companies that carried out social actions for the benefit of communities. It is estimated that approximately 600 thousand companies act voluntarily, considering the universe of 871 thousand formal companies in Brazil

SOCIAL RESPONSIBILITY

DEFINITION

The concept of Corporate Social Responsibility raises the issue of the company’s relationship with its various stakeholders, as expressed in the definition of the Ethos Institute:

“Responsabilidade social empresarial é a forma de gestão que se define pela relação ética e transparente da empresa com todos os públicos com os quais ela se relaciona e pelo estabelecimento de metas empresariais compatíveis com o desenvolvimento sustentável da sociedade, preservando recursos ambientais e culturais para as gerações futuras, respeitando a diversidade e promovendo a redução das desigualdades sociais” (ETHOS, 2008).

Corporate Social Responsibility generally involves the search for new opportunities as a way of responding to the environmental, social and economic demands of the market. Within the concept of Corporate Social Responsibility that has been incorporated by companies, the target audience is no longer just the consumer and starts to encompass a much larger number of people and companies influenced by the organization’s actions. This Social Responsibility is part of sustainable development, which comprises the economic, environmental and business dimensions, thus contributing to the improvement of society’s quality of life. A presentation of this concept is the following definition:

“A responsabilidade social nasce de um compromisso da organização com a sociedade, em que sua participação vai mais além do que apenas gerar empregos, impostos e lucros. O equilíbrio da empresa dentro do Ecossistema social depende basicamente de uma atuação responsável e ética em todas as frentes, em harmonia com o equilíbrio ecológico, com o crescimento econômico e com o desenvolvimento social.” (BARBOSA and RABAÇA, 2001 apud TENÓRIO, 2006, p.25):

The company inserted in this concept will be more participatory with society, its function being more complete, in addition to the economic role it plays. Thus, expanding its performance and at the same time valuing it as an agent of transformation.

Social Responsibility involves some topics, Oliveira (2002):

- Vision and Mission;

- Ethic;

- General human resources practices;

- Labor/union relations;

- Health;

- Relationship with the production chain;

- Shareholder relationship;

- Market practices;

- Customer service;

- Social marketing;

- Social balance;

- Relationship with government;

- Environment;

- Cultural actions;

- Community support;

- Human rights.

With basic skills and social responsibility, companies acquire the respect of communities and consumers that influence their activities, increasing recognition for all employees that result in a competitive advantage for the organization itself, valuing its brand, image and giving greater credibility.

THE SOCIAL RESPONSIBILITY POLICY

According to Martins (2008), a company focused on performing as a socially responsible organization in social and environmental terms, mobilized towards the ideal of sustainability, has as one of its great challenges to write a document, the Social and Environmental Responsibility Policy, known as RSA. .

Following ethical principles, its actions are written based on and inspired by its own strategic business roots, with perspective and focus on its audiences:

- Suppliers;

- Customers;

- Consumers;

- Environment;

- Community;

- Government and society in general.

And based on these elements, the company directs its principles, including in its strategy:

- Company mission: Description of the company’s commitment to its employees and society by offering services and increasing their value;

- Vision: Related to its area of activity, presents its objective and purposes;

- Values: achievement in practices and actions that demonstrate which behaviors society has. Some of them are quality, trust, excellence, security, respect and justice;

- Code of ethics: Based on the mission, vision and values, it is the set of posture and the way the organization operates. Being the basis for knowing if the image is in accordance with its own identity, helping to resolve moments of impasse and crisis.

THE SOCIAL RESPONSIBILITY POLICY AND ITS PERFORMANCE

In an annual report, the company expresses all its actions, objectives and philosophy, demonstrating its value to society.

Included in the mission, vision and values are all investments in projects in each area of its public. In which the financial statement of these shows the social balance of the company, dividing its projects into four aspects, among them:

- Employees: inclusion of people with disabilities, apprentices, seniors, career plans, positive work environment, appreciation of diversity and CIPA’s;

- Environment: technologies to save water, avoid waste of plastic cups, reuse of paper as drafts, tree planting campaigns and garbage selection;

- Community: Investment in education and art, organization of social fundraising parties, helping to distribute food and clothing to homeless people;

- Society: reduction of child labor, cooperation between NGOs and unions, helping with education projects, lectures on sustainable topics and volunteering for social actions.

SOCIAL BALANCE

The purpose of this report is defined by Luca (1998):

“[…] atender às necessidades de informações dos usuários da contabilidade, no campo social. É um instrumento de medida que permite verificar a situação da empresa no campo social, registrar as realizações efetuadas neste campo e principalmente avaliar as relações ocorridas entre o resultado da empresa e a sociedade” (LUCA, 1998 p.32).

One of the ways the company demonstrates its social performance is through the publication of the social report.

It is a statement that is presented along with the company’s financial statement annually. It presents information such as a description of the enterprise profile, the economic sector in which it operates, company history, structure, principles, values, mission and policies.

The balance sheet content is expressed in its indicators, such as social, internal, external, environmental, structure and social responsibility indicators. The information is aimed at the company and employees, the environment, community and society.

Some companies, analyzing the return that they have when applying these concepts and with their results, invest in social marketing, as they increase recognition, profit from the brand and image through the news broadcast. But the important thing is the internal recognition, because it is what motivates employees for being involved with social causes, being a promoter of the company and one of the ways is the implementation of the SA8000 Standard. Oliveira (2012).

According to The Social Balance and the Company’s Communication with Society 5 ed, page 20, the table presents factors that show the company’s participation in social issues as shown below:

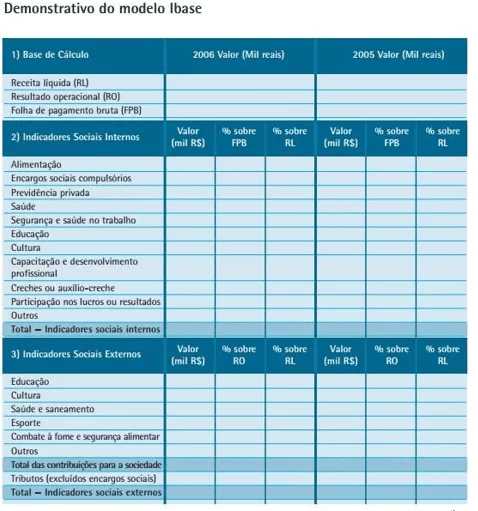

Table 1 – Social Balance Model presented by the Ethos Institute

The model proposed by IBASE must contain the following information:

1- Calculation Basis: information corresponding to net revenue; the operating result presented by the organization and the gross payroll accounted for in the period.

2- Internal Social Indicators: information related to the company’s social actions carried out together with its employees (food, private pension, health, education, culture, training and professional development, day care or daycare assistance, profit sharing or results, among other benefits ).

3- External Social Indicators: information corresponding to the company’s social actions carried out in partnership with society (comprises the total contributions to society plus taxes, excluding social charges).

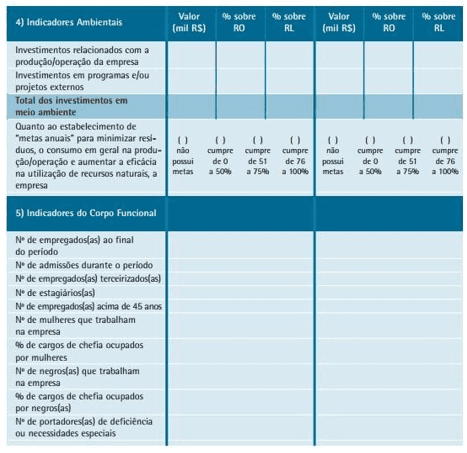

4- Environmental Indicators: operational information of the company that involves the environment, that is, how much was invested to recover what was harmed by it. These 7 investments refer to external projects such as depollution, conservation of environmental resources, ecological campaigns, as well as investments for the continuous improvement of environmental quality in the company’s production, such as expenses with the introduction of non-polluting methods, environmental audits, among others.

5- Staff Indicators: information on employees (number of women working in the company, number of blacks, number of interns, number of employees over 45 years of age, among other indicators of the staff).

6- Relevant information: regarding the exercise of corporate citizenship and a questionnaire related to employee participation in social responsibility actions carried out by the company.

7-Other Information: this space is available for the company to add other important information regarding the exercise of social responsibility, ethics and transparency.

In relation to volunteer work, according to Fischer and Falconer (2001) in Corporate Volunteering – Business Strategies in Brazil.

“A maioria das empresas que consolidaram sua atuação social constituiu um instituto ou uma fundação, como forma jurídica e organizacional mais adequada para gerir as atividades. Estão nesse caso, na amostra estudada, o Instituto C&A, o Instituto Credicard, a Fundação Iochpe, a Fundação Victor Civita, a Fundação Educar e a Fundação Acesita. Enquanto Natura, Xerox, Avon, Informare, Dixtal, Bosch, McKinsey, Caixa Econômica Federal, Intermédica, 3M, Andersen Consulting e Schering-Plough são empresas que mantêm as atividades sociais no próprio âmbito da organização.” (FISCHER and FALCONER , 2001, p.5)

Thus, many institutions and foundations dedicated to social responsibility in Brazil are maintained and managed by multinationals or national companies, such as those mentioned above, and information can also be found at the Institute for Research, Promotion and Inspection of Social Responsibility.

PRESENTATION OF THE RESEARCHED COMPANIES

BANCO DO BRASIL

It was founded in 1808 by Prince Regent D. João, when the country became the seat of the Portuguese Crown.

In 1821, it became linked to the Brazilian capital market, being in 1905 the majority shareholder in the Federal Government and in 1906 with public listings on the Stock Exchanges.

In 1945, he was responsible for paying Brazilian troops, transferring money and attending to the country’s embassy.

In 1960, it transferred its headquarters to Brasília.

In 1985 he created the Banco do Brasil Foundation and opened the Banco do Brasil Cultural Center a year later. It launched the internet portal in 2000 and 2002, adapted the bylaws for the adoption and transparency of social practices and in 2011 it acquired Banco da Patagonia.

And in 2014, it revised its mission, vision and values of its corporate strategy with the principle of being a market bank with public spirit.

Today it is a bank with greater service in the country and abroad, with 99.8% in the municipalities and 60.1 thousand service points and in 135 countries with agreements with other banks, today it is controlled by the Union since 2006 on the BM&FBOVESPA market.

C.E.F. (CAIXA ECONÔMICA FEDERAL)

Founded in 1861 by D. Pedro II, called Caixa Econômica da Corte, with the purpose of encouraging savings and granting loans under pledge, guaranteed by the government.

In 1931, it inaugurated consignment loan operations for individuals, where it later assumed the exclusivity of this activity.

In 1886, the bank merged with BNH, Banco Nacional de Habitação, in which it was the largest financing agent for home ownership, urban development and basic sanitation. With the extinction of the BNH in the same year, it became the main Brazilian Savings and Loan System (SBPE), managing the FGTS and funds of the Brazilian Housing System, where in 1990 it began to centralize the FGTS accounts of 70 banking institutions. In 1961 it created the Federal Lotteries, in 1969 it became a public company with its obligations and duties of a social nature and in 2013 it started artistic, cultural, educational and sports initiatives in Brazil.

Today it is consolidated in the market as a large company, the main agent of public policies of the federal government. It has 62,406 points spread throughout Brazil and branches in more than 20 countries.

ANALYSIS OF THE COMPANIES’ SOCIAL BALANCE SHEET

The Social Balance of the two banks were analyzed in a comparative way between the years 2013 and 2014. The Annual Sustainability Report and Social Balances published by the banks can be accessed on the website of each one that demonstrates their actions and investments in detail, containing the sources of information regarding the development of its social activities in the internal and external context, relevant to the exercise of citizenship, being published annually with financial statements for the same period.

Next, the two Social Balance Sheets are analyzed, comparing the indicators released in the years 2013 and 2014.

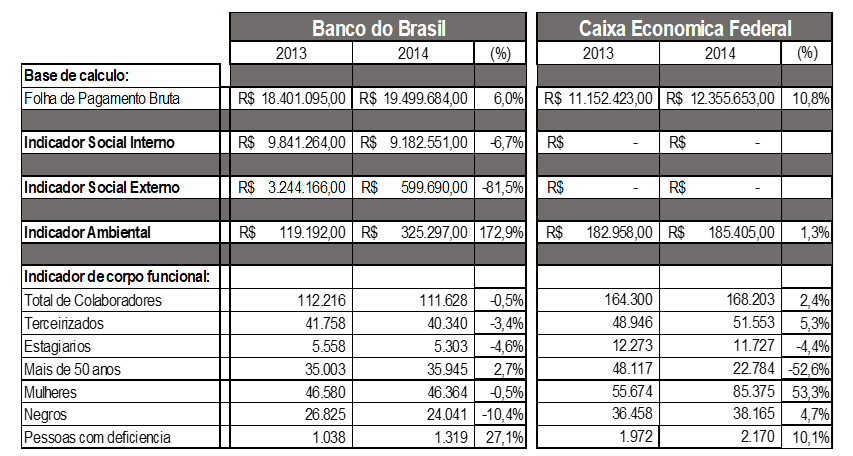

Table 1 – Comparison of the 2013 and 2014 social balance of the institutions Banco do Brasil and Caixa Econômica Federal

CALCULATION BASIS

Referring to Table 1, from 2013 to 2014, the payroll of Banco do Brasil increased by 6%, while Banco Caixa was 11% more, between 2013 and 2014

INTERNAL SOCIAL INDICATORS

Banco do Brasil, having reduced its investments in the internal social indicator by 6.7%, was the smallest decrease compared to the external social indicator.

Caixa Econômica, which was surveyed, did not provide complete or easily identifiable information, and could not be compared in the year or with another institution.

EXTERNAL SOCIAL INDICATORS

From 2013 to 2014, there was a decrease in investment in social indicators by 81.5%, realizing that the focus was on the importance of the environmental factor, related to Banco do Brasil. Caixa Econômica Federal does not provide information related to this Research Indicator.

ENVIRONMENTAL INDICATORS

As shown in the information on the respective Social Balance, Banco do Brasil, emphasizing the social sphere, increased its indicator to 173%, unlike Caixa, which was only 1%, maintaining the average in the comparison period.

FUNCTIONAL BODY INDICATORS

The total number of employees in this period differed differently between each company, with a decrease of 0.5% at Banco do Brasil and an increase of 2.4% at Caixa Econômica.

Outsourced employees and service providers had a decrease of 3.4%, while in the other bank, there was an increase of 5.3%.

The vacancies of interns had a decrease with similar numbers, of 4.6% compared to a number of 4.4%.

Employees over 50 years old, the 2.7% increase at Banco do Brasil is compared to a considerable difference in the 52.6% decrease in vacancies at Caixa Econômica.

Regarding the number of women in the company, there was a negative difference of 0.5%, and with a different proportion, 53% more than in 2013.

Blacks had a big drop of 10% in the first bank and in the other, an increase of 5%.

People with disabilities were more important for Branco do Brasil, with increases of 27% and 10% in Caixa.

When analyzing the topic of diversity, Caixa Econômica Federal has a greater number of employees than Banco do Brasil, with blacks being the largest number, with a difference of 14,124 employees, together with women who have almost half with 39,011 employees and people with disabilities with 1,132 employees. Unlike those over 50, who have 13,161 fewer employees.

FINAL CONSIDERATIONS

In this research, there is a deep knowledge of sustainability and social responsibility, referring to the concept and historical process of technical research, analyzing the way that companies employ their actions in their corporate policy, aiming at benefits to collaborate with society and the environment, as well as generating value for investors and shareholders.

Regarding the analyzed companies, it appears that among them there are projects in several social areas, acting internally and externally.

Information on the company’s social responsibility can be found on its own website, which discloses its social balance sheets referring to its indicators.

It is also clear that the social balance in each one of them shows transparency with its information, which can sometimes be very detailed, making analysis difficult.

BIBLIOGRAPHIC REFERENCES

ADCE/UNIAPAC BRASIL. Carta de princípios dos dirigentes cristãos de empresa. Salvador, 1965.

ASHLEY, Patrícia Almeida (coord.). Ética e Responsabilidade social nos negócios. São Paulo: Saraiva, 2002.

ATKWHH, Instituto. As metas do milênio da ONU.

BRASIL, Banco do. Balanço social 2014. Disponível em: <http://www45.bb.com.br/docs/ri/ra2014/pt/11.htm>. Acesso em: 17/10/16

BNDES. Balanço da implementação da PRSA 2015-2017. Disponível em: <https://www.bndes.gov.br/wps/wcm/connect/site/06130b22-68a4-4a85-b5be-731cbe6dc931/Relatorio_PRSA_2015-2017.pdf?MOD=AJPERES&CVID=meElwW3>. Acesso: 29/11/17

CAIXA ECONÔMICA FEDERAL, Banco. Balanço Social 2014. Disponível em: <http://www.caixa.gov.br/Downloads/caixa-relatorio-sustentabilidade/Relatorio_de_Sustentabilidade_2014.pdf>. Acesso em:17/10/16

CAIXA ECONÔMICA FEDERAL. Sobre a Caixa econômica federal. Disponível em: <http://www.caixa.gov.br/sobre-a-caixa/Paginas/default.aspx>. Acesso em: 29/10/16

CONSULTORIA, Dialogus. Abordagem Conceitual e Histórica da Responsabilidade Social Empresarial. Disponível em: <https://www.dialogusconsultoria.com.br/abordagem-conceitual-e-historica-da-responsabilidade-social-empresarial/>. Acesso:18/10/2016.

DALBERIO, Osvaldo; DALBERIO, Maria Cecília Borges. Metodologia Científica: desafios e caminhos. São Paulo: Paulus, 2009.

ETHOS, Instituto. Balanço social e a comunidade da empresa com a sociedade.

FIGUEIREDO, Nébia Maria Almeida de (org.). Método e metodologia na pesquisa científica. 2ª edição. São Caetano do Sul, SP: Yendis Editora, 2007.

FISCHER, Rosa Maria & FALCONER, Andres Pablo. Voluntariado empresarial estratégias de empresas no Brasil. Revista de Administração da USP (RAUSP), v.36, n.3, p.5, julho. /setembro de 2001.

FREIRE, F.S.; SILVA, C.A.T. (Org.) Balanço Social: teoria e prática. São Paulo: Atlas, 2001.

GUIMARÃES, T. N; LEITE FILHO, G. A. Empresas modelo versus empresas não modelo de responsabilidade social: um estudo comparativo de indicadores econômico-financeiros no período de 2001 a 2004. 2006. 48f. Tese.

IBASE. Balanço social. Disponível em: <https://ibase.br/pt/balanco-social/>. Acesso em: 18/11/2016.

IBGE. Estimativa de população.

LUCA, Márcia Martins Mendes. Demonstração do Valor Adicionado. São Paulo: Atlas, 1998.

MARTINS, José Pedro Soares; Responsabilidade social corporativa: como a postura responsável pode gerar valor. São Paulo: Komedi,2008

NOVAES, Washington. Eco-92: avanços e interrogações.1992. 15f. Artigo-São Paulo,1992

OLIVEIRA, Marco Antonio Lima de. SA 8000: o modelo ISO-9000 aplicado à responsabilidade social. Rio de Janeiro: Qualitymark, 2002.

PNUD. Objetivos do desenvolvimento sustentável. Disponível em: <http://www.br.undp.org/content/brazil/pt/home/sustainable-development-goals.html> Acesso:17/10/16

SAI. Social Accountability Internacional. Norma SA8000. Disponível em: <http://www.sa-intl.org/_data/global/files/SA8000Standard_Portugues(1).pdf>. Acesso: 11/03/19

SEVERINO, A. J. Metodologia do trabalho científico. 23 ed. rev. e atual. São Paulo: Cortez, 2007.

TENÓRIO, F. G. Responsabilidade social empresarial: teoria e prática: Rio de Janeiro: FGV, 2006.

UFSC. Análise de Responsabilidade social: estudo comparativo de duas instituições financeiras.

UNDP. Brasil. Disponível em: <http://www.br.undp.org/content/brazil/pt/home/countryinfo.html>. Acesso: 27/11/16

APPENDIX – FOOTNOTE

2. Association of Christian Business Leaders – Brazil.

3. Brazilian Institute of Social and Economic Analysis.

[1] MBA in Strategic and Business Management – USCS – University of the Municipality of São Caetano do Sul and BA in Business Administration – UNIABC – Universidade do Grande ABC.

Sent: March, 2018.

Approved: May, 2019.